Smart Contract-Driven Data Trading: The Full Pipeline from Authorization to Settlement

Tens of billions of data interactions happen on the internet every day — users browsing, publishing content, clicking recommendations, filling out forms. But the ownership confirmation, authorization management, and value settlement that should accompany all of that data relies almost entirely on centralized platforms and manual legal processes. A single data transaction, from seller authorization to buyer settlement, has to thread its way through user agreements, API terms of service, data use agreements, reconciliation cycles, and bank clearing. The pipeline is long enough to generate friction, disputes, and trust costs at every step.

Under this model, data trading is essentially governed by humans. What smart contracts can change is replacing every step in that pipeline — every step that currently depends on manual judgment or institutional backing — with code-driven, immutable, automatically executing contract logic.

We’re building exactly this kind of end-to-end smart contract system inside the MEMO ecosystem. It isn’t a single standalone product. It’s an automated data trading engine composed of three core components — the DataDID identity system, the ERC-7829 data asset standard, and the data marketplace — working in concert. This piece follows a real data transaction from authorization through asset formation, matching, and settlement, unpacking the contract logic at each layer.

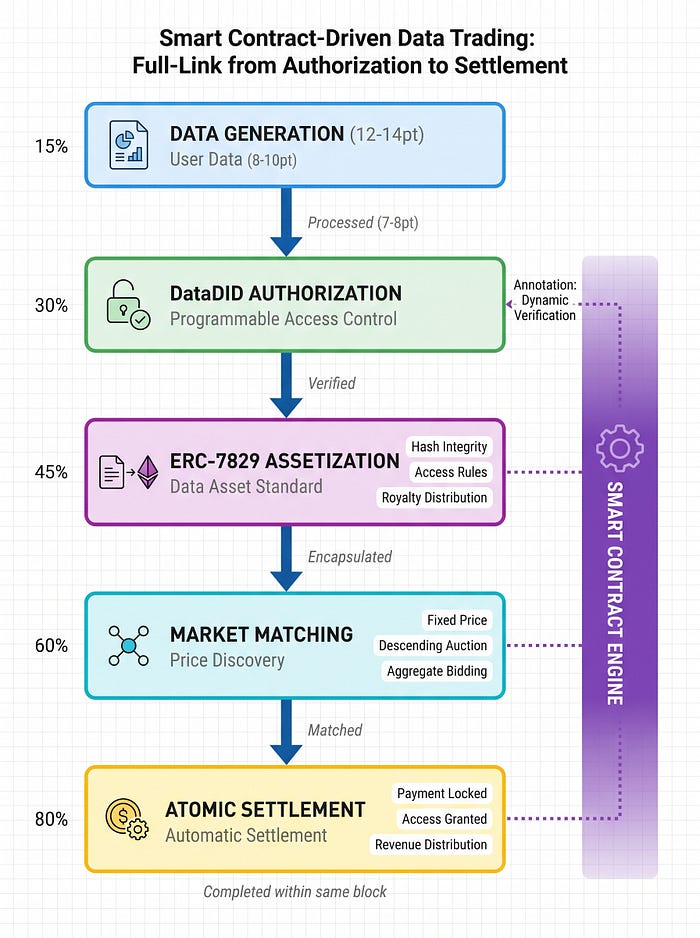

Step One: Authorization

When a user decides to make a category of their data available for trading, what does that decision look like on-chain?

In the traditional model, “authorization” is a legal document — the user checks an “I agree” box, legal effect is created, but technical enforcement is completely decoupled from it. The platform has the authorization, but how the data gets used, by whom, and how many times is invisible and unauditable to the user.

DataDID’s authorization model moves this on-chain. Every authorization decision isn’t a binary “agree/disagree” — it’s a set of programmable access control rules, encoded directly into the user’s DID contract. Rules can specify who can access the data, whether access is one-time or within a time window, whether what’s being accessed is an aggregated statistical signal or a de-identified structured record, and whether payment is required and at what amount.

A concrete example: a user can allow an AI training data aggregator to access their browsing behavior category signals for 30 days, at no more than 0.01 USDT per call — while explicitly excluding raw browsing history and any information linkable to personal identity. That rule isn’t written in terms of service. It’s written on-chain. When the aggregator’s contract initiates an access request, the system automatically checks whether the user’s authorization rules in the DID contract cover the current request. If the rules don’t match, access is blocked at the contract layer — no human review required.

This transforms authorization from “a one-time upfront permission” into “per-call verification at the moment of access.” The user doesn’t need to trust any intermediary — only the contract itself. And the contract code is publicly auditable.

Step Two: Asset Formation

Once authorization is established, the user’s data needs to be encapsulated as a standardized asset that can be traded in a marketplace.

This is precisely what ERC-7829 is designed to do. The minting contract, upon receiving a user’s Mint request, executes three actions.

First, it computes a cryptographic hash of the data content and writes it as an integrity proof into the token’s on-chain storage slot. This guarantees the asset’s authenticity: at any subsequent point in the trading pipeline, anyone can verify whether the asset has been tampered with simply by comparing the on-chain hash against the data content they hold.

Second, based on the distribution strategy the user specifies at mint time, it configures the token’s access control rules. These rules determine how the asset circulates in the marketplace — publicly readable but requiring payment for commercial use, restricted to specific buyers, or open for competitive bidding.

Third, it encodes the user’s revenue split ratio into the contract’s royalties field — for example, 90% of primary market sales to the data provider and 10% to the protocol, with 5% of each secondary market transfer going back to the original creator.

The moment minting completes, the data is no longer a passive sequence of bytes. It’s a self-contained, self-verifying on-chain asset with its own trading rules and revenue logic built in.

Step Three: The Marketplace

The central design challenge for the data marketplace’s matching layer isn’t transaction speed — data assets aren’t high-frequency trading instruments that need millisecond latency. It’s price discovery and eliminating information asymmetry.

In traditional data trading, pricing is the biggest black box. Sellers don’t know what their data is worth. Buyers don’t know whether data quality justifies the asking price. Information asymmetry means sellers get lowballed, buyers end up with data that doesn’t meet expectations, and market efficiency suffers across the board.

Our marketplace contract introduces an on-chain price discovery mechanism. When listing data, providers choose from three pricing modes.

Fixed price: a set unit price and available quantity, first come first served. Dutch auction: price decreases over time until someone bids — designed to resolve seller uncertainty about market acceptance. Pooled bidding: multiple buyers jointly bid for aggregated usage rights to the same category of data; the top N bidders receive authorization and settle at their actual bid price.

Each mode corresponds to an independent set of contract logic, deployed automatically at listing time with no manual intervention during execution. Buyer bids, seller acceptance, price discovery, and trade matching all complete inside the contract. Every bid and settlement record is publicly queryable. Anyone can build their own pricing models from historical transaction data. Pricing transparency goes from zero to complete.

Step Four: Settlement

This is the highest-automation step in the entire pipeline, and the one that most clearly illustrates what smart contracts replace in the traditional model.

In conventional data trading, settlement means the buyer confirms receipt of the data, runs it through internal review, initiates a wire transfer, and the seller waits 3 to 15 business days for bank clearing. If the parties are in different jurisdictions, add cross-border payment fees, exchange rate exposure, and compliance review time. Settlement costs frequently run 5–10% of transaction value, and funds in transit generate no value for anyone.

In the smart contract settlement layer, payment, delivery, and revenue distribution are three atomic operations that complete within the same block.

The buyer’s payment is locked in an escrow contract in stablecoins. Once the smart contract verifies that the buyer’s bid matches the seller’s listing price, it calls the ERC-7829 asset’s access control interface to open read permissions for the buyer’s address. Once the permission-granted event fires, the escrow contract automatically distributes the funds: the split specified in the royalties field routes automatically to the data provider’s address, the protocol treasury address, and any upstream contributor addresses. The entire pipeline, from buyer confirming a bid to seller receiving funds, takes no longer than one contract interaction’s gas confirmation time.

No wire transfer. No manual review. No bank clearing window. No trust required from any party. The contract logic is transparent, the distribution outcome is auditable, and every fraction of every payment has an on-chain record.

For a complex transaction involving multiple upstream contributors — say, a dataset that passed through a collector, an aggregator, and a quality reviewer before reaching the end buyer — the four-way revenue sharing agreement and monthly finance reconciliation cycle of the traditional model gets executed by a smart contract in a single block. Every participant receives their payment precise to the wei level, under distribution rules that were locked at the moment the data asset was minted and that no party can modify after the fact.

A Complete Transaction, End to End

Put all four steps together and a real transaction looks like this.

A user has registered a DID identity in DataDID and accumulated a batch of browsing behavior signal data through the Data Mining module. They decide to list this data for sale — they initiate a listing in the data marketplace, choose fixed price mode, and set 5 USDT per dataset.

The ERC-7829 minting contract executes immediately: computes the data hash to generate an integrity proof, configures access control according to the user’s authorization rules (commercial use only, non-exclusive), and encodes a 90% user / 10% protocol revenue split into the contract.

After listing, a procurement contract from an AI training data aggregator matches the listing. The aggregator confirms the price and sends 5 USDT to the escrow contract. The smart contract verifies three things in sequence: whether the aggregator’s DID identity is on the authorized allowlist, whether the payment amount matches, and whether the data integrity proof is valid. Once all three pass, the contract automatically grants the aggregator’s address data read permissions, transfers 4.5 USDT to the user’s wallet, and routes 0.5 USDT to the protocol treasury.

The entire process — from the user clicking “list” to funds arriving in their wallet — involves four contract interactions: the DID authorization contract, the ERC-7829 asset contract, the marketplace matching contract, and the settlement escrow contract. But the user doesn’t need to know any of those contracts exist. From the user’s perspective, there are two steps: list, get paid.

That is what end-to-end smart contract-driven data trading looks like as a product experience.

Where Things Stand

This system is still in active development. DataDID and ERC-7829 are already running in production. The data marketplace’s core contracts are in internal testnet feedback iteration. The first half of the pipeline — authorization through asset formation — is fully operational. The second half — matching through settlement — awaits final technical validation once the marketplace launches publicly.

But the direction is clear.

When data ownership is confirmed by an on-chain DID, data asset formation is guaranteed by the ERC-7829 standard, and data trading and settlement execute automatically through smart contracts — “data as an asset” stops being an abstract industry narrative. It becomes a precisely defined entity at the contract layer, one that can be created, held, traded, and settled on a blockchain.

For the first time, every step between data generation and data monetization has a chance to be compressed into a single body of publicly auditable code. No platform dependency. No legal dependency. No banking dependency.

That change affects more than data trading efficiency. It affects the question that the internet industry has failed to answer for twenty years: who owns data, who controls it, and who profits from it.

DataDID is MEMO’s decentralized data identity system, with over one million registered users. ERC-7829 was proposed by the MEMO team and has been adopted by over 20 projects. The data marketplace is in active development.

👉 datadidapp.memolabs.net